Summary of misstatements

Als onderdeel van de einddocumentatie voor een opdracht kan het nodig zijn dat je een evaluatie geeft van de afwijkingen die tijdens de controle zijn geïdentificeerd. Je opdrachtdossier kan een rapport bevatten met de naam Samenvatting van onjuistheden.

Dit document bevat automatisch informatie die relevant is voor je evaluatie:

-

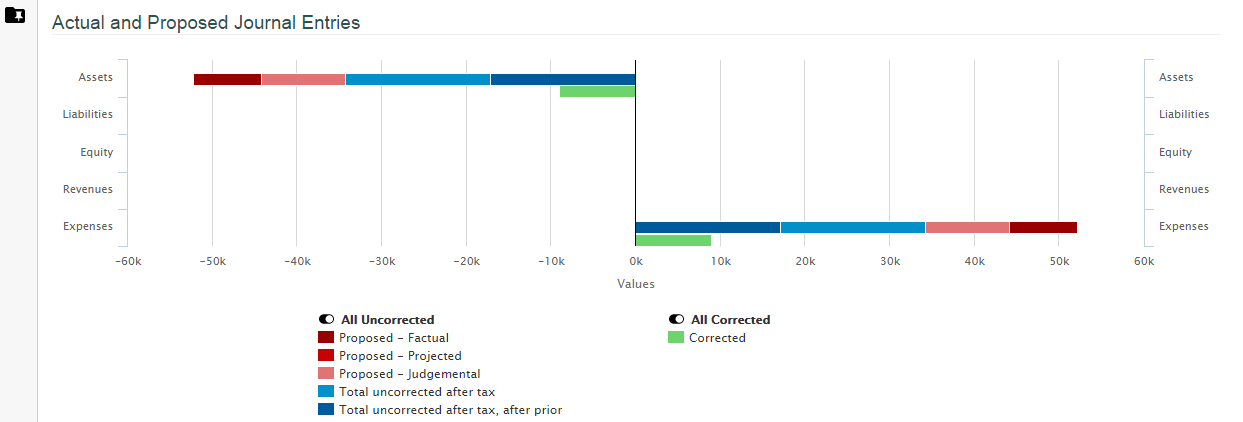

Het gedeelte Werkelijke en voorgestelde journaalposten geeft alle aangepaste en voorgestelde journaalposten weer in de vorm van grafieken.

-

Het gedeelte met kerngegevens geeft bepaalde gegevens weer over de algehele betrokkenheid en materialiteit.

Je kunt het geschatte effectieve belastingtarief invoeren.

-

Het gedeelte Samenvatting van onjuistheden in de jaarrekening bevat een tabel met alle financiële groepen met onjuistheden en een uitsplitsing van de bedragen van de onjuistheden.

Onder deze secties kun je je evaluatie van de onjuistheden opschrijven. U kunt ook alle weggelaten openbaarmakingen toevoegen, inclusief of deze al dan niet zijn gecorrigeerd en de redenen waarom ze niet openbaar zijn gemaakt.

Zodra je klaar bent met de evaluatie van de onjuistheden, kun je je conclusie presenteren - of de niet-gecorrigeerde verschillen over het geheel genomen materieel zijn of niet - en het document aftekenen.