Risks and estimates

![]()

Dit artikel betreft Caseware Audit.

Complete the documents in the Pervasive risks and Estimates folders in the following sequence:

- 506 Identifying fraud risks

This is a standard checklist document with procedures to help you identify any possible fraud risks based on information known up until this point in the engagement. - Proceed to 508 Assessment of business and fraud risks - Worksheet

The first section of this document titled Business risks and fraud risk factors and possible responses (PEG 508) has a preset list of possible business and fraud risk factors that you can select from, categorized into different groups. For each of these groups, there is also a preset list of possible management responses that may address the risk factors identified. Lastly, there is a Response and comments column where you can add any additional details not covered by the preset items.

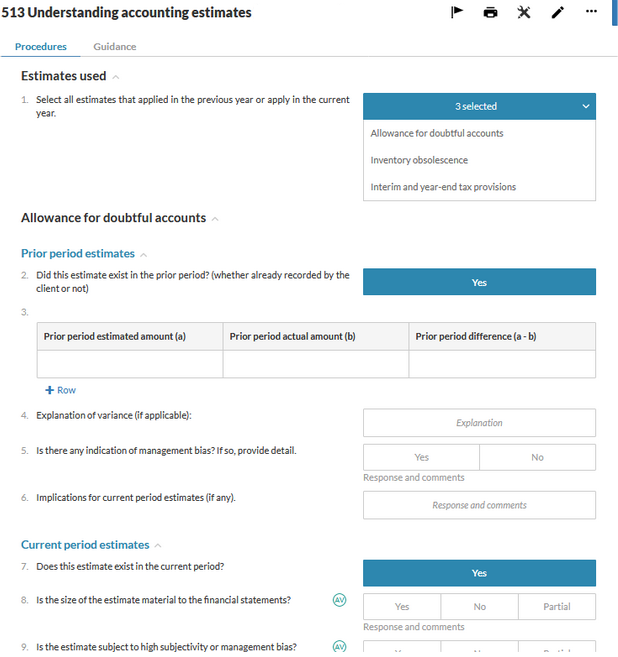

The second section of this document titled Fraud scenarios (PEG 437) has a preset list of potential fraud scenarios and reasons that might exist (attitudes/rationalizations or incentives/opportunities), that you can select from. There is also a column for each where you can document other details on the possible scenarios. - 513 Understanding accounting estimates

This document contains a preset list of common estimates found in audit engagements, that you can select from, as well as an Other option.

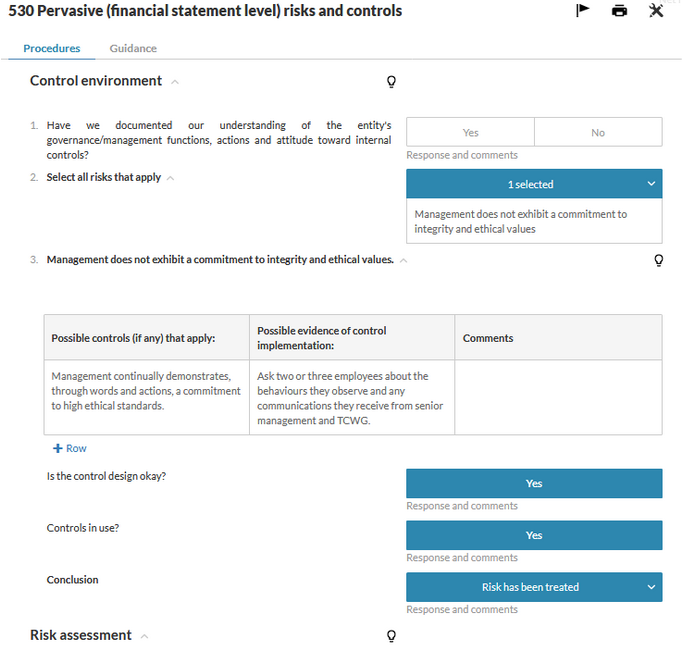

- 530 Pervasive (financial statement level) risks and controls

This document includes a preset list of risks that may exist across the entity as a whole where you can select any that exist and are relevant. For any selected, a preset list becomes visible where you can determine if any possible controls apply related to the risk and if there is any possible evidence of control implementation.

- 540 Financial statement level and assertion level risks listing Note

The link to this document, in the Next step area of 530 or from the Documents page, links you to the Risks tab at the top of the engagement.

This is where you can see all created risks, create new risks, link the risks to areas of the engagement where they were identified and where they will be addressed, and conclude on risks to ensure they have been addressed. This is a key page that drives much of the audit work to be performed.