Materiality and risk assessment

![]()

Dit artikel betreft Caseware Audit.

Complete the documents in the Materiality and Risk assessment folders in the following sequence:

- 419 Possible misstatements in qualitative disclosures

Use this document to determine:

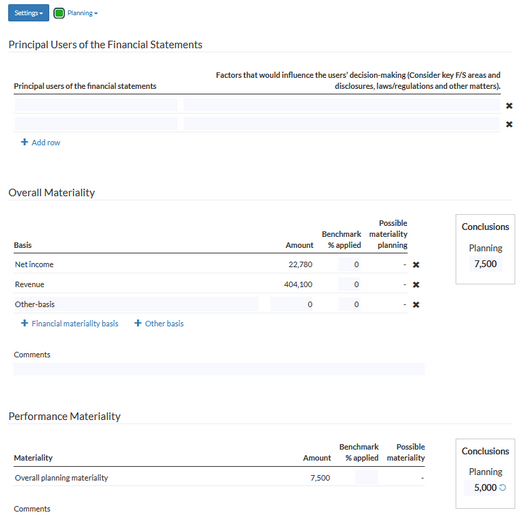

- Overall materiality (including possible misstatements in qualitative disclosures) based on the users of the financial statements (CAS 320.10).

- Performance materiality required to reduce (to an acceptably low level) the probability that the aggregate of uncorrected/undetected misstatements exceeds overall materiality (CAS 320.11).

- Specific materiality and specific performance materiality where required (CAS 320.10 and .A11-A12). - Materialiteit

Use this to document who the principal users are, and calculate how they will determine materiality and performance materiality, as well as what defines a trivial misstatement, and if materiality and performance materiality are needed for any specific circumstances.

The amount set as the planning materiality in the first "Conclusions" box and the amount set as the planning performance materiality in the second "Conclusions" box will become visible in the top right of the engagement next to the + button, underneath Net Income.

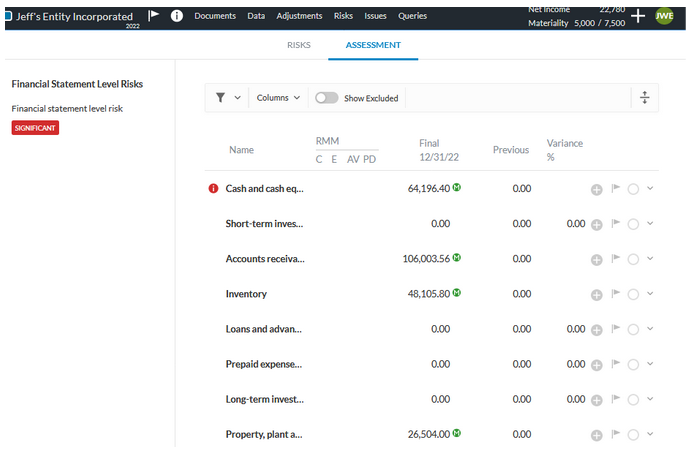

The amount set for materiality has a large impact on how the engagement is performed. It is one of the key tools used by auditors to plan their audit and response to risks. All of the individual work programs (for example, A Cash and cash equivalents, C Accounts Receivable) have a visibility condition so that they become visible if the total amounts in the trial balance for that area exceed the amount set as the planning materiality.

In addition, the risk assessment performed further along in the engagement will have "M" symbols visible next to each financial statement area that exceeds materiality in order to guide you in planning your audit response.

- Risicobeoordeling

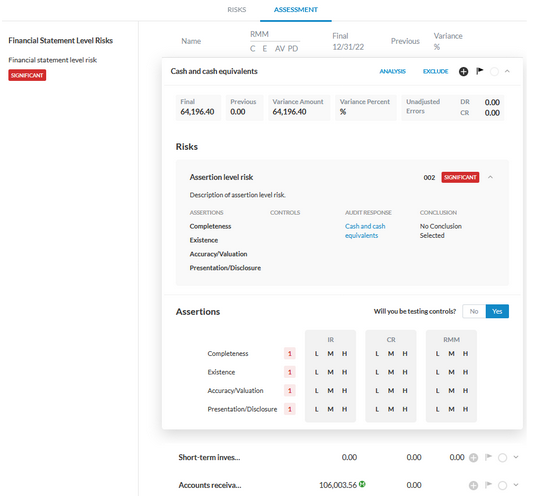

As shown in the image above, each financial statement area is shown on the risk assessment page. This page is another import "hub" or "summary" of the engagement, and is where you will plan most of how you will respond to your identified risks. This is done by taking into account factors such as:

- Is the financial statement area material?

- Have any risks been identified in the engagement that affect the specific financial statement area being assessed?

- If so, does it increase the audit risk of material misstatement (RMM) for that area?

You can use this to document your assessment of risk levels by financial statement areas based upon all information gathered up to this point, both financial and from the Risk Identification and Assessment phase documents. - 605 Responding to risk at the financial statement level

This is a standard checklist with some procedures on responding to risk at the financial statement level.